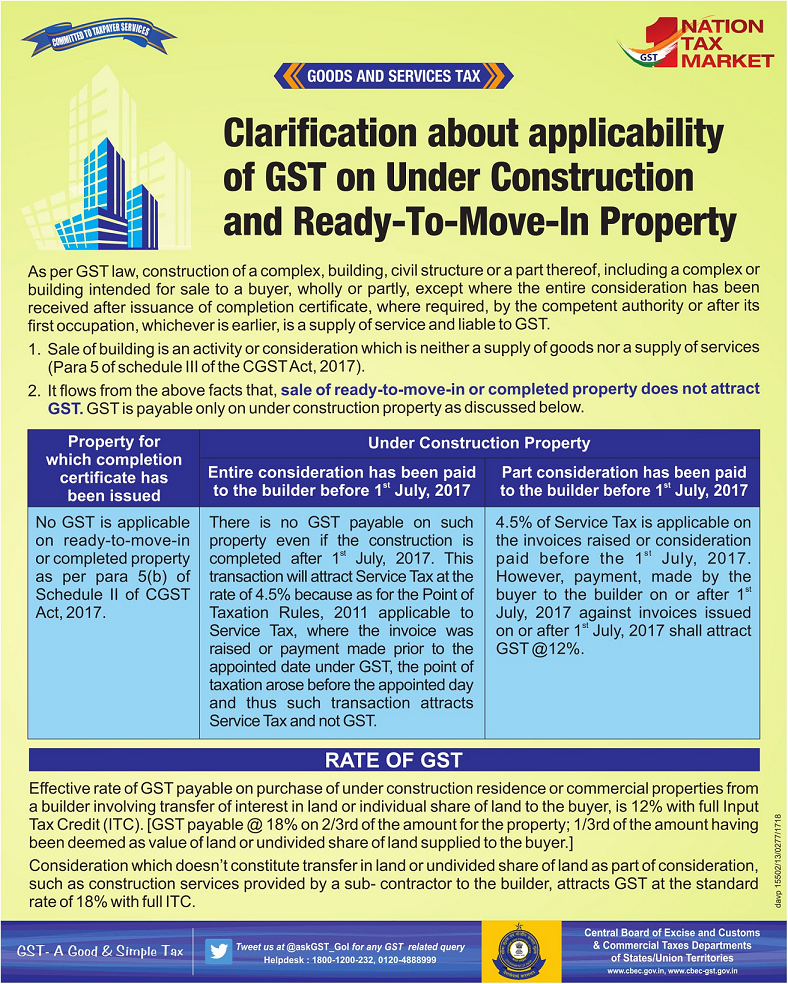

GST Rate On Real Estate:

Real estate sector will invite GST at the rate of 12 per cent with full input tax credit. According to the schedule of GST rates for services as approved by the council, real estate sector will comprise “construction of a complex, building, civil structure or a part thereof, intended for sale to a buyer, wholly or partly. The value of land is included in the amount charged from the service recipient.” These will be charged @ 12 per cent with full input tax credit. In other words, it means all under-construction properties will invite a GST of 12 per cent. However, GST will not be applicable for ready-to-move-in properties.

However, there are still some variations for under-construction properties and confusion regarding the same.

There are various stages for under-construction properties and GST will be dependent on it.

When You Have Bought A Property After The Completion Certificate Was Issued To The Builder:

In such a situation, GST will not be applicable as it is considered a ready-to-move-in property and there is no transfer or supply of goods and services.

Payment Made To The Builder In Part Or In Full Before The Roll Out Of GST Regime:

Whether you paid in part or in full, if the payment is made before the roll out of GST regime, then it will not invite any GST tax. However, keep in mind that you will be charged applicable service tax rate of 4.5 per cent.

GST On Under-construction Flats, Properties Or Commercial Properties:

In this category, the actual GST rate is 18 per cent. But one-third of this 18 per cent is deemed as the value of land or undivided share of land supplied to the buyer of the property. Hence, GST rate lowers down to 12 per cent on under-construction flats, properties or commercial properties with full input tax credit.

GST On Resale Properties Or Flats:

As they are considered ready-to-move-in properties, they will not invite GST taxation